My Clients Don't Have Any Money

Living most of my life in Florida, cockroaches were a fact of life. In general, if you spotted one cockroach, that meant there were at least 1,000 others somewhere, waiting in the wings.

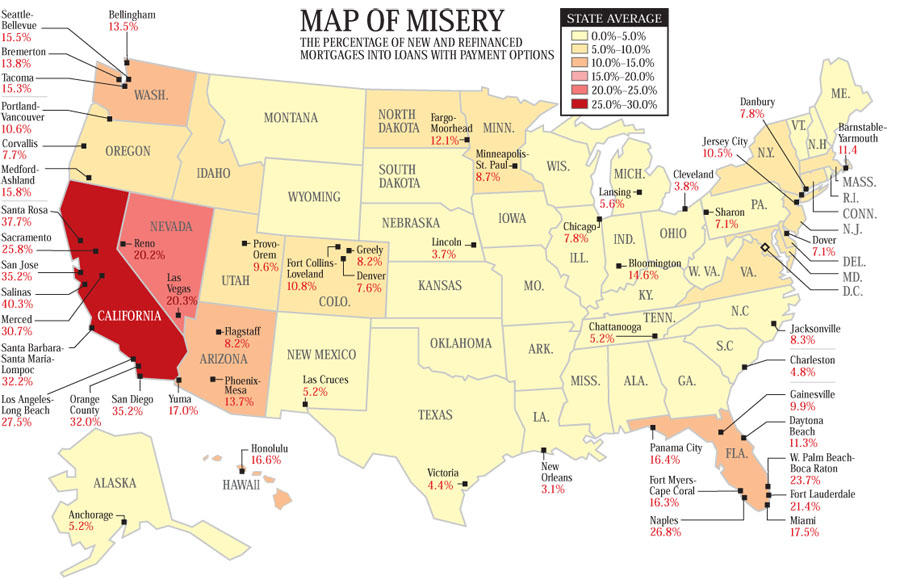

In the past few months homeowner subprime sob stories have been coming at us from all over the country, ad nauseam. With Washington state in the top five for toxic loans, you'd figure we'd see more local stories.

Here's one from the Seattle Times this morning: Borrower, beware: Debt disaster looms as rates rise on easy-money mortgages

It was a sweet little house, with affordable day care nearby for their 6-year-old son. Patrick Fultz and Laurel Swartz were hooked.Editors note: Always watch your back when a commissioned salesperson beings a sentence with "I help"

But when the couple — with no savings and about $20,000 in credit-card debt — shopped for a mortgage to buy their 1,200-square-foot house in Tukwila last year, they heard the same thing from lenders and in a home-buying class they attended: Forget it.

"You basically had to be Scot free, no massive credit debt, which we had, and to have money in the bank, which we didn't," said Swartz, 31. "How do people buy houses in America anymore?"

Fultz thought he had found just what he was looking for when he came across Gold Mortgage Lending in Renton on the Internet. "No income verification mortgage, zero down," read the firm's Web site. "We fund mortgages the others can't."

Erin Rearden, a mortgage counselor at Solid Ground, a nonprofit social-service agency in Seattle, said the deal Fultz and Swartz struck is typical, especially as the cost of housing skyrockets out of reach for so many.

"They wanted a home. And a lot of this comes from operating under the assumption that owning a home is an inherent American right. So when someone offers a way to do it, you want to go for it," she said.

Fultz makes $12.75 a hour driving a fish-food delivery truck. He recently paid off half of the 12 credit cards he used in buying a motorcycle, a couch and a television, going out to eat, "just buying stuff," Swartz was working at an insurance office, where she made $11.75 an hour.

The couple signed two mortgages to buy their $246,800 house in July. The first loan, a so-called pick-a-payment loan for 80 percent of the deal, had a variable interest rate. The second mortgage, at 12.5 percent interest, covered the rest.

Not long after they signed the loan, Swartz decided to dump her sedentary office job to become a personal fitness trainer. The new job paid less, $7.89 an hour, but she had the opportunity to earn commissions as she brought in clients.

The commissions, however, didn't materialize. At the same time, the interest rate on the first mortgage went up, from 7.06 to 8.15 percent — and it can go up every month until topping out at 11.5 percent.

Suddenly the couple were $300 a month short of paying their bills.

"I feel sorry for anyone who can't get into a house," Mills said. "We beg the banks to give us their turn downs. I help people; that's the bottom line."

But today, people like Fultz and Swartz aren't the only ones having money problems. Mills, and brokers like her, have troubles of their own.Wait a minute... I'm confused. I thought your customers were people that already didn't have any money? Or were you talking about the money to pay your broker fees?

A meltdown in the subprime lending market is drying up the money pipeline.

Across the country, where home values are stalled or plummeting, lenders are watching loans turn upside down, with mortgages grown larger than property values. People behind in payments are losing their homes. Entire neighborhoods in parts of the Midwest and California are shuttered by bad debt.

The situation is nothing like that in Seattle, where increasing home values can still grease the mechanics of subprime deals.

But even here, lenders have stopped serving subprime clients or are imposing tighter requirements to qualify, from higher credit scores to a couple of months' worth of payments in the bank and at least some money down.

"For my clients, that is a deal killer," Mills said. "My clients don't have any money."

The pullback has cratered the business model for brokers like Mills. She used to write 10 to 15 loans a month. In March, she wrote two. In February? None.While the map of misery shows a percentage of toxic loans of roughly 15%, I wonder how many of these loans were written in just the last year or so?

"I didn't make my own mortgage payment this month," Mills said in April. "But nobody feels sorry for me."

Where will future "buyers" get the money for even a 5% down payment. If there are less buyers, what will that do for Seattle home values?

Now that we've seen one homedebtor facing foreclosure story here in Seattle, I wonder how many other stories are out there?

(Lynda V. Mapes, Seattle Times, 05-07-2007)

{kind=link}

21 comments:

You basically had to be Scot free, no massive credit debt, which we had, and to have money in the bank, which we didn't,"

Has anyone else ever thought about the semantics of debt? People frequently refer to debt as something they "have". It seems it might be less scary to think of your self as "having" 20K of debt, than to think of yourself as "owing" 20K.

Anybody have any thoughts on this?

Why rent? To get richer

http://tinyurl.com/2a4d69

BTW, I have nearly given up on Seattle. I have my family there and have thought about moving back, but my wife's family is in Minneapolis, and it is looking better everyday. I just can't take LA much longer.

"How do people buy houses in America anymore?"

You know, I read this article stupified... for starters when some one signs away their financial life yet knows not what "negative amortization" means when their names is on the friggin' documents is BEYOND BELIEF!!!

there's the internet and wikipedia, easy 'nuff to look up neg-am.

And this is why I have little if no sympath for the people that got themselves into trouble and why my Democrat leanings are taking a back seat to my Libertarian views about 'caveat emptor'...

Its really hard to suffer fools in our day and age. Come on, its the 21st century people, "the Quick (of mind)and the Dead". It doesnt' take that much to put some brain power to use to diseminate what you're signing.

And for the "How do people afford houses?" nonesense? Well dude, its called prudence, saving and discipline. I know, friggin' carzy I realize, but sometime you have to WAIT for what you want. These are people whose parents never made them save allowance to score the Millenium Falcon playset.

So here's my answer, "How do people afford houses(with a combined income of <$20/hr)?".... they don't!

The critical distinction that was left out of the article is that Tukwila is not Ballard.

If Ballard were a video Ipod, Tukwila would be a Zune. There isn't any possible comparison.

What sort of bizarro world do these people live in where "owning" or living in a house is some sort of right?

It's not like they are lacking shelter. These (ignorant) people are being preyed upon by lenders/real estate hucksters who feed them the image that home ownership is some sort of civil right.

Now I understand that you can't just lay claim to a piece of land, start cutting trees, and raise yourself a log cabin anymore, but there is ample evidence on this blog and elsewhere that there is no shortage of housing (ie, rentals) in this region.

Maybe the world has changed and it's not normal to have to be gainfully employed and financially responsible for _years_ to be able to afford a house. Apparently now it's a human right to be able to get a mortgage right out of high school?

Mike --

You're forgetting something: it's products like the Zune (and several reported sales of Boeing's outsourced jets) that prove beyond a reasonable doubt that this region's economy is bulletproof, headed for the moon, and the median income is headed for 100k, with house prices averaging $750k in the next year.

Special!

Gee, they bought last year. Why don't they just take their massive appreciation and cash out?

I had the misfortune of having to go to Southcenter this weekend - the place was jam-packed. Hard to even find a place to park. Based on that view it is hard to believe the economy is slowing down. Probably all clones of this couple on a credit-card fueled buying binge.

Tim said: "With Washington state in the top five for toxic loans, you'd figure we'd see more local stories."

Ummm, I think this is mis-leading. Sure, Washington state has a high number of exotic mortgages, but we are actually pretty low in the sub-prime category. The chart Tim links to doesn't differentiate between sub-prime and prime, it only talks about the exotic loans types (e.g. 100% interest, option ARM, etc). It's important to remember that not all these new-fangled loans are sub-prime.

This goes a long way to explaining why the Puget Sound isn't seeing a blow up of the same magnitude as elsewhere (i.e. because we have relatively few sub-prime loans). However, I agree that in the long run most of these exotic mortgages will blow up. But not right now. The first class of loans to crater is the sub-prime type. When the next foot falls, and Alt-A generally goes up in flames, THEN we can expect to read a lot of horror stories in the local press.

Tim said...

Please take note, just under the headline of this post: posted by synthetik.

Are there any exact stats on where we rank with subprime?

I don't think it matters much - even if we don't rank high in subprime (which we probably do), there will be even more fallout from the rest of the lending suite of goodies.

Nothing will save us it's just a matter of how long we can prolong the process.

Kind of like oil depletion.

Person making $100,000+/year, with $100,000+ in savings: WTF? I can't afford these prices.

Person making $30,000/year with massive consumer debt: I DESERVE IT!

Are there any exact stats on where we rank with subprime?

I remember reading that CSFB report on mortgages - and our market wasn't even on the chart showing % of mortgages that were subprime. Since the chart only went down to the average in the market, I infered that Seattle must be below average.

My favorite detail from this story: the "helpful" mortgage broker was sitting in a leopard-print chair....

Classy. Was she wearing a pinky ring, too?

synthetik said: "Are there any exact stats on where we rank with subprime?"

I saw some a couple months ago, but am not sure where. If I recall correctly, the something like 8% or 9% of the Seattle area mortgages were sub-prime, which was far lower than many places in California, Florida, and elsewhere, that had upwards of 20% sub-prime.

What this data did NOT tell us was how this trended historically. Maybe 8% is very high for the Puget Sound.

In any event, I agree that we will feel pain here eventually, and that the massive rise in the use of exotic loans is ample evidence that the bubble has struck the Puget Sound with a vengeance. However, we won't feel the impacts of the downturn until the credit tightening moves further up the food-chain, hitting Alt-A.

Tim said: "Please take note, just under the headline of this post: posted by synthetik"

I appologize for the mis-attribution. I don't know why I got my wires crossed.

Subprime crisis not big threat: Buffett

The Oracle speaks, but says nothing we haven't heard before:

House prices fell at their fastest pace in 13 years in February, according to the S&P/Case-Shiller home price index, which was released in late April. The slowdown, combined with an increase in interest rates in recent years, has triggered turmoil in the subprime mortgage business, which lends to poorer home buyers with blemished credit records.

Borrowers and lenders in the subprime mortgage business were betting that house prices would go up in future, Buffett said. Now that delinquencies and foreclosures are increasing there's extra supply of homes for sale, which changes the dynamics of the real estate market, he explained.

"You'll see plenty of misery in that field. You've already seen some," Buffett said. "I don't seen a big impact on the economy though."

So, according to Mr. Buffett, there won't be blood in the streets when the national (including Seattle) real estate bubble deflates.

Full Article

You know I'm becoming an Aubrey fan more and more... check out the disparity in the Times vs. PI headlines...

King County home prices keep rising, bucking national trend

-The Rhodester

Home prices remain steady

-Aubrey

I'm wondering if Ms. Rhodes has a leapord print high-back in her office their at the Times building as well

Person making $100,000+/year, with $100,000+ in savings: WTF? I can't afford these prices.

Person making $30,000/year with massive consumer debt: I DESERVE IT!

Ain't that the truth.

I went to a small college. Many of my fellow students were from 100 year old money. Family names we would all recognize.

The funny thing was, most of them drove complete beaters if they had a car at all. Many had side jobs. They were humble, hard-working individuals.

Not too hard to see how the money grew generation to generation.

How about the fact that these buyers went to several lenders who told them no...they kept on searching until they found someone happy to take advantage.

Plus, the brand new home buyer decided her dependable salary job was boring and became a commissioned fitness trainer.

Where is the accountability? Maybe we should be using IQ tests instead of FICO scores.

I'm not defending the LO. I think it's terrible she put them in an option ARM with 100% financing.

The pullback has cratered the business model for brokers like Mills. She used to write 10 to 15 loans a month. In March, she wrote two. In February? None.

"I didn't make my own mortgage payment this month," Mills said in April. "But nobody feels sorry for me."

That's because you're the bad guy. We cheer when the bad guy loses. That quote and the "How do people buy houses in America anymore?" quote are simply AMAZING.

"She used to write 10 to 15 loans a month. In March, she wrote two. In February? None."

waa waa.

I will bet she made more than 1.5 on each subprime loan she did during her "harvesting" months. And now she's crying she can't make her payments after two tough months...would you go to Kathy Mills for your next mortgage (she seems to be the alpha dog)??

http://www.gold-mortgage.com/meetourstaff.html

Post a Comment